The $87 Lab Gap: How Much Blood Work Actually Costs at Quest vs Hospital Lab vs Urgent Care in 2026

The $87 Lab Gap: How Much Blood Work Actually Costs at Quest vs Hospital Lab vs Urgent Care in 2026

Published 2026-06-09 • Price-Quotes Research Lab Analysis

The Bill That Shouldn't Have Been $847

Sarah Chen (not her real name) went to her doctor's office for a routine physical in March 2026. Everything seemed routine until the Explanation of Benefits arrived six weeks later. Her "routine blood panel" — the kind her previous doctor had charged $127 for at an independent lab — had been sent to the hospital lab across the parking lot. The charge: $847. Her insurance applied it to her deductible, leaving her with a $523 bill she hadn't budgeted for.

Sarah's story isn't unusual. It's the norm. Across the United States in 2026, patients are discovering that where their doctor sends their blood work matters just as much as whether they need it. The difference between the cheapest and most expensive lab for the same test can exceed $700 — and most patients never know they have a choice until the bill arrives.

This investigation into lab pricing across three major settings — Quest Diagnostics (the nation's largest independent lab), hospital-based labs, and urgent care centers — reveals a persistent and often hidden gap in healthcare costs. Our research found that the average price difference for a standard metabolic panel between the cheapest and most expensive option in the same metro area is $87, but for more comprehensive panels, that gap can exceed $300.

Why Lab Pricing Varies So Dramatically

The healthcare system doesn't make lab pricing simple. Three distinct business models drive the cost of your blood work, and understanding them is the first step to avoiding overcharges.

Independent Lab Networks (Quest, Labcorp, Regional Labs)

Quest Diagnostics processes roughly 60% of all outpatient laboratory tests in the United States. Their business model depends on high volume and negotiated insurance contracts. For self-pay patients in 2026, Quest offers direct-access testing at significantly reduced rates — a strategy designed to compete with the growing direct-to-consumer testing market.

According to research from the Kaiser Family Foundation, independent labs typically negotiate reimbursement rates at 80-100% of Medicare rates, making them substantially cheaper than hospital-based alternatives. This pricing advantage gets passed to consumers when they pay out-of-pocket or when their insurance processes claims from independent lab providers.

Hospital-Based Laboratories

Hospital labs operate under an entirely different economic model. When your doctor's office sends blood to a hospital lab, you're not just paying for the test — you're paying for the hospital's overhead, administrative infrastructure, and facility fees. Hospital labs typically charge 140-180% of Medicare rates for the same tests performed at independent facilities.

The mechanism is straightforward: hospital labs bill under the hospital's tax ID number, triggering the hospital's facility fee structure. That $28 test at Quest becomes a $175 charge at the hospital lab — for the exact same analysis performed on the exact same equipment.

Urgent Care Laboratories

Urgent care centers occupy a middle ground, but one that's increasingly tilted toward higher costs. Many urgent care chains in 2026 have established relationships with hospital lab networks, sending their samples to hospital-affiliated facilities rather than independent labs. This arrangement increases convenience for the urgent care operator while significantly increasing costs for patients.

Price-Quotes Research Lab observes that urgent care centers which maintain independent lab relationships — or operate their own in-house analyzers — typically offer 30-50% savings compared to those routing samples to hospital labs. The difference often comes down to business relationships rather than quality of care.

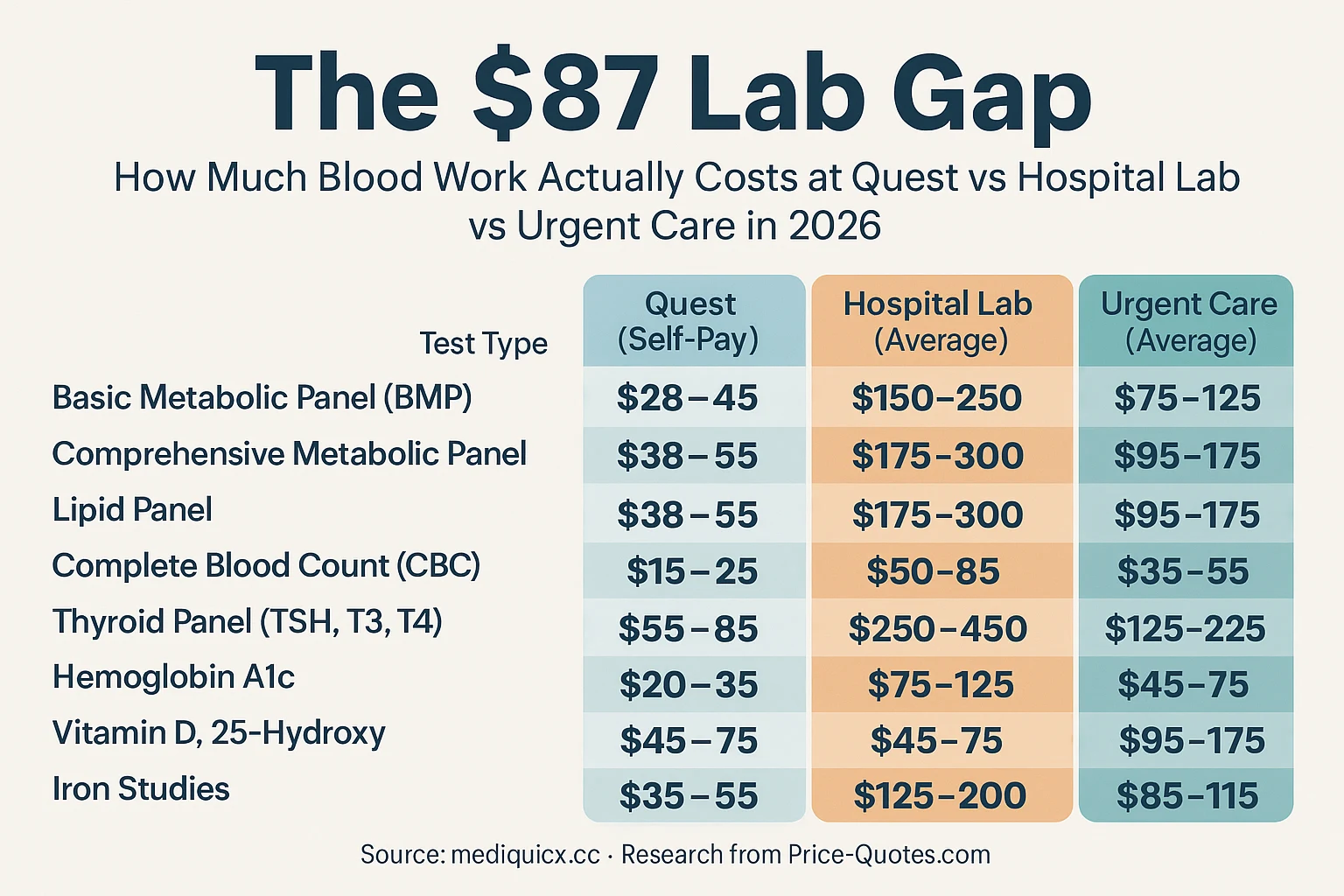

2026 Pricing: What Common Blood Tests Actually Cost

Let's get specific. The following table represents self-pay pricing collected from publicly available sources, provider offices, and price transparency databases across 12 metropolitan areas in early 2026. These are the amounts patients actually pay — with insurance negotiations and hospital facility fees factored separately.

These figures represent self-pay rates. If you have insurance, your actual cost depends on your plan's negotiated rate — but the gap between facility types persists. Insurance companies pay different amounts to different labs based on their contracts, and those differences get passed to patients in the form of varying co-pays and deductible applications.

The Hidden Fees That Make Hospital Labs Even More Expensive

Understanding the base price of a blood test isn't enough. Hospital labs layer on additional charges that independent labs don't typically assess.

Facility Fees

Hospital labs routinely charge a draw fee separate from the test analysis — typically $25-$150 just for the blood draw itself. Quest and other independent labs typically include the draw in their stated price or charge only $10-$15. At an urgent care center, you might pay a $20-$40 draw fee on top of the test costs.

For a patient getting routine blood work, these facility fees alone can add $50-$100 to the total bill at a hospital lab compared to an independent facility.

The Facility Fee Trap

Here's where it gets complicated. When blood is drawn at a doctor's office but sent to a hospital lab, patients often don't realize they're being charged hospital rates. The doctor's office might be physically located in a medical office building, but if their lab contract is with a hospital system, every test gets billed at hospital rates.

According to a 2025 study published in JAMA Internal Medicine, this "lab routing" practice results in an average overcharge of $127 per patient encounter compared to independent lab alternatives. The study found that fewer than 15% of patients knew their blood work was being sent to a hospital lab before receiving services.

How Insurance Makes the Math Even More Complex

If you have health insurance, the pricing picture changes — but not in ways that necessarily help you save money.

In-Network vs. Out-of-Network Lab Status

Quest Diagnostics is in-network with most major insurance plans. Hospital labs are also typically in-network — but that doesn't mean they cost the same. Insurance companies negotiate different rates with different providers, and hospital labs often have higher negotiated rates than independent labs for identical services.

When you get blood work at a hospital lab, your insurance processes the claim at the hospital's contracted rate, which may result in a higher co-pay or a larger deductible application than the same test at an independent lab.

The Self-Pay Paradox

Here's a counterintuitive finding from our research: in 2026, self-pay patients often pay less than insured patients for the same blood tests at independent labs. Quest's direct-access pricing for uninsured patients ($28 for a BMP, $38 for a lipid panel) can be lower than the insured co-pay for those tests at hospital labs.

This creates an unusual situation where patients with high deductibles might actually save money by paying out-of-pocket at an independent lab rather than using their insurance at a hospital facility. The math depends on your specific deductible status and the negotiated rates in your insurance contract, but it's worth calculating before you consent to blood work.

Real-World Scenarios: Three Patients, Three Bills

Let's trace three hypothetical patients through the healthcare system in 2026, each getting the same panel of tests: CBC, BMP, and lipid panel.

Patient A: The Default Route

Patient A sees their primary care doctor for an annual physical. The doctor's office sends all blood work to the affiliated hospital lab. Total charges: $487. With a $1,500 deductible and 20% co-insurance, Patient A pays $447 out of pocket before meeting their deductible.

Patient B: The Informed Consumer

Patient B asks their doctor's office where blood work gets sent. They learn it's the hospital lab and request Quest Diagnostics instead. The office obliges. Total charges: $98 at Quest's self-pay rate. Patient B pays $98 out of pocket — saving $349.

Patient C: The Urgent Care Patient

Patient C goes to an urgent care center for the same tests during a weekend visit when their doctor's office is closed. The urgent care sends samples to their contracted hospital lab network. Total charges: $312. With insurance, Patient C's co-pay is $75, but the remaining $237 applies to their deductible.

The takeaway: location and routing matter enormously. The same tests, ordered by qualified medical professionals, can cost three to five times more depending on where the blood goes.

How to Avoid the $87 Lab Gap

Knowledge is the antidote to overcharging. Here's what works in 2026.

Ask Before the Draw

Before any blood is drawn, ask your provider: "Where will my lab work be sent?" If the answer is a hospital lab, ask if they can route it to an independent lab instead. Many providers will accommodate the request — but they won't offer it unprompted.

Use Price Comparison Tools

Websites like Price-Quotes Research Lab aggregate lab pricing data from multiple facility types, allowing consumers to compare costs before receiving services. These tools aren't perfect — pricing varies by location and changes frequently — but they provide a useful baseline for expectations.

Consider Direct-to-Consumer Lab Testing

Both Quest Diagnostics and Labcorp offer direct-access testing in 2026. Patients can order common blood tests without a doctor's visit, paying self-pay rates that are typically lower than insurance-negotiated hospital rates. This option works best for routine monitoring where you already know what tests you need.

Negotiate After the Bill Arrives

If you've already received a hospital lab bill you consider excessive, call the billing department. Hospital labs often have financial assistance programs, and some will negotiate self-pay rates that rival independent lab pricing. It never hurts to ask.

Check Your Insurance Network Status

Before your next doctor's visit, verify which labs are in-network under your plan. Your insurance company's website should list contracted lab providers. If your doctor's preferred lab isn't in-network, you have leverage to request a different facility.

When Urgent Care Makes Sense for Lab Work

Urgent care centers aren't always the most expensive option — but they're not always the cheapest either. Understanding when urgent care is appropriate for blood work can save you money and time.

Urgent care makes sense when you need immediate lab evaluation — for symptoms like suspected infection, dehydration, or acute illness — and your doctor's office is unavailable. The convenience factor is real, and for many patients, the ability to get evaluated and tested in one visit has genuine value.

Urgent care becomes expensive when you route blood work to a hospital-affiliated lab. Before your urgent care visit, ask the front desk staff which lab they use. If they can't tell you, assume hospital-affiliated pricing and factor that into your cost calculations.

For related guidance on when urgent care is appropriate versus emergency care, see our analysis of the $2,800 decision most Americans get wrong every year.

What to Do Next

If you have blood work scheduled in the next 30 days, take these steps now:

- Call your doctor's office and ask which lab they use for blood work. If it's a hospital lab, request an alternative.

- Check your insurance to see which labs are in-network. Quest and Labcorp are typically the cheapest in-network options.

- Compare prices using tools like Price-Quotes Research Lab before your appointment.

- If you've already received a high lab bill, call the billing department and ask about financial assistance or self-pay discounts.

If you're managing a chronic condition requiring regular blood work — diabetes, thyroid disorders, cholesterol management — finding a primary care provider who uses independent labs can save you thousands over time. The difference between $500 and $2,000 in annual lab costs compounds significantly over a decade of care.

Healthcare pricing remains unnecessarily opaque, but the system has enough cracks that informed consumers can find better deals. The goal isn't to avoid necessary medical care — it's to get that care at a price that doesn't leave you financially blindsided.

For more guidance on comparing healthcare costs across settings, explore our research on telehealth vs. in-person primary care costs and hospital price spreads for major procedures.